Is ECO Crop Insurance Worth It?

Considerations for growers regarding the problems of the Enhanced Coverage Option.

By Jeremy Petree

Most farmers are familiar with Federal Multi Peril Crop Insurance (MPCI) programs that protect their crop by paying a loss if their harvested production and revenue drops below a certain percent of their historical average. As a crop insurance agent with 15 years in the industry, I can tell you that these yield and revenue protection policies are by far the most popular, most tested, and most reliable policies available. However, in recent years there have been several new products made available that pay based on the county’s production and revenue instead of the individual’s.

The Enhanced Coverage Option, or ECO, is one such product. It’s still heavily subsidized, but unlike the most common crop insurance policies that typically cap out at the 85% level, ECO begins to trigger if the county averages below 95% of its expected production and/or revenue and pays up to 9% of the farmer’s expected crop revenue. While your production history is used to calculate your guarantee, it does not affect whether or not an ECO loss is triggered. You may have a bumper crop but still get a payment from an ECO policy simply because the rest of the county had a below average year.

It may sound like a no brainer at first glance, but is ECO really a good buy?

The problem with ECO is that when it doesn’t pay, you’re paying a high premium for a product that isn’t directly protecting your investment.

In western North and South Carolina, 75% Enterprise Unit with revenue coverage on corn can cover you for as much as $400/acre for less than $7 or $8/acre. Coverage is closer to $250-$300 on soybeans and wheat, but premiums are still less than $9 per acre. ECO costs roughly the same amount as an underlying 75% level but pays out a maximum of $30 to $45 per acre on a complete payout. That’s only around 12% of the maximum amount that your underlying policy would pay if you harvested nothing.

In a year where the stars align and you have a great season but the county struggles, the ECO payout can be a windfall. Likewise, in a bad year when you collect on your policy and the county is below 95% of their average, the ECO money would be welcome. The problem with ECO is that when it doesn’t pay, you're paying a high premium for a product that isn’t directly protecting your investment. You may have a claim on your crop, but if the county does well, you still have to pay the ECO premium, which means less money to keep you going to the next year.

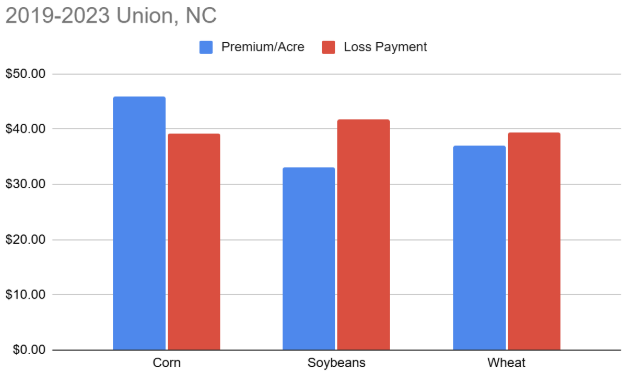

ECO has only been around for a few years, but yearly county yield and revenue data exists for other area based crop insurance purposes, so it’s simple enough to figure out when ECO would have paid out in the past. RMA hasn’t determined 2024 final yields and revenue but I’ve made the following calculations based on Union County, NC 2025 estimated premium and coverages. Consequently, dollar amounts below are just approximations, but the general trends in Premium vs. Loss Payment should be accurate.

Typically, you can increase your underlying coverage from 75% to 80% for less than the cost of adding ECO to your policy.

As you can see from the graphs below, if we go back to 2021 using the data available, ECO costs more money in premium than it pays out for growers in Union, NC for all three major grain crops. Going back to 2019 and then 2017, the premium to loss ratio is more favorable for corn and soybeans, but it’s quite a bit of money to shell out year to year to only net $15-30/acre. Most of the ECO indemnity would have paid out in 2018 and 2019. For the other five years, the grower would have been paying $7-$9/acre for a product that paid nothing even if they had a poor harvest. The 2017-2023 premium to loss ratio for Union County wheat didn’t even break even.

Three Years

Five Years

Seven Years

Premiums and ECO payments can vary significantly from county to county, but the general trend I’ve shown above for Union County, NC repeats itself in other counties across the region. Typically, you can increase your underlying coverage from 75% to 80% for less than the cost of adding ECO to your policy. It’s 4% less in dollar coverage than you get by adding ECO, but it costs less and specifically protects your investment in your crops rather than gambling on the county’s success or struggle.

I think it’s generally a mistake to think about insurance in terms of “How often does this have to pay for me to not be wasting money.” After all, this is risk management, not financial planning, and you’re always better off making a good crop and not needing to use the insurance. But you have to recognize that a 10 bushel corn loss or a 4 bushel soybean loss would pay out more than ECO and that the cost of increasing your personal coverage by that much would be the same or less than adding ECO.

…would you rather have spent $4… and have another $20-$30 of coverage on your crop, or spend $8 for another $45 in coverage that will depend of how your neighbor’s season goes?

ECO has to pay out in full around once every 5 years for you to break even . To get your premium back on a 75% Enterprise Unit with Revenue Protection, it only needs to pay out about half once every 20 or 25 years simply because every dollar buys you that much more insurance.

In a bad year, when you need to collect, would you rather have spent $4 to raise your coverage to 80% and have another $20-$30 of coverage on your crop, or spend $8 for another $45 in coverage that will depend on how your neighbor’s season goes? If you do choose to put your money with ECO, will you have time to wait for the payment to come through? As of writing this in late January, 2025, last year’s wheat crop has been harvested for more than six months and we still don’t know if there will be an ECO payment. How quickly do you think you’d need the money?

Am I telling you not to even consider buying ECO? No, of course not. No one has a better idea of what’s best for your operation than you do. However, I do think you should seriously consider the bigger picture when looking at an area coverage product. Make sure the crop that you put out is protected before you start spending money on county level coverage.

…opting for ECO over increased base coverage, at least to me, seems to be missing the forest for the trees.

In North and South Carolina, we don’t see much ECO on spring crops because of the availability of the Hurricane Insurance Protection and Wind Index (HIP-Wi) which cannot be bought if you have ECO. However, some agencies have been pushing ECO on wheat as we don’t see many hurricanes and tropical storms come through the area that would trigger a payment on wheat. It’s easy to get drawn in by high numbers when it comes to coverage, and you may find yourself thinking ECO is a way to a huge payout. And over the long run, years or even decades, that may be true. Because of the way crop insurance is rated and subsidized, you’re likely to get more out of it than you spend over a long period of time.

But farms aren’t hedge funds and most farmers don’t have thousands of dollars to throw into a program that may or may not produce long term gains. It’s one thing to buy a rainfall index program on a handful of farms as an investment tool where the premiums are reasonable and the data is consistent over, 5, 10, and 20 years, but opting for ECO over increased base coverage, at least to me, seems to be missing the forest for the trees.

Protect your operation first and look at an area plan as a type of investment to consider if you have the extra resources to spend on it. Ask your agent questions like, “How many times would ECO have paid out in this county and for this crop in the last three years; The last seven?” I like to think I work in an honest industry with good people, but always remember that your agent makes a little commission for every dollar that you spend. I would be hard pressed to sell ECO to a grower that I wasn’t sure had considered all the options, and I would consider it unconscionable to push someone to buy it knowing it would have barely paid out in the last seven years. Ask yourself, “Is it really better for my operation to spend money gambling on the county, or should I save some money and maximize the amount I get when my farm is having trouble?”

The goal of buying crop insurance should first and foremost be to keep you going to the next year no matter how bad a season you have. Know what your goals are and what you’re buying and always keep the big picture in mind. It’s always up to you how to spend your money, but don’t miss the forest for the trees.